1 Introduction

1.1 What is Agency Banking?

Agency Banking enables you to provide your customers with a GBP bank account number and sort code or an EUR bank account number and IBAN, which they can use to easily make top-up payments via the banking network to fund their payment cards. Your customers can also use the solution to transfer funds out of their card account. Payments into the account can be made via Faster Payments![]() These are payments between banks made using the UK Faster Payments scheme, which supports near immediate payment., SEPA

These are payments between banks made using the UK Faster Payments scheme, which supports near immediate payment., SEPA![]() The Single Euro Payments Area (SEPA) makes European payments as easy as payments made in the UK. A SEPA payment takes about 24 hours, so is not as quick as Faster Payments., BACS

The Single Euro Payments Area (SEPA) makes European payments as easy as payments made in the UK. A SEPA payment takes about 24 hours, so is not as quick as Faster Payments., BACS![]() Bankers Automated Clearing System (BACS) is an electronic system for making payments directly from one bank account to another, such as bank-to-bank transfers. Bacs payment services are operated and managed by Bacs Payment Schemes Limited, a membership organisation consisting of 16 of the UK's leading banks. Thredd supports BACS payments using our Agency Banking service. and CHAPS

Bankers Automated Clearing System (BACS) is an electronic system for making payments directly from one bank account to another, such as bank-to-bank transfers. Bacs payment services are operated and managed by Bacs Payment Schemes Limited, a membership organisation consisting of 16 of the UK's leading banks. Thredd supports BACS payments using our Agency Banking service. and CHAPS![]() Clearing House Automated Payment System (CHAPS) is typically used for one-off, high-value payments that need to be sent and received on the same day. There is usually a fee associated with CHAPS payments.. Payments out of the account can be made via Faster Payments, SEPA and Direct Debit.

Clearing House Automated Payment System (CHAPS) is typically used for one-off, high-value payments that need to be sent and received on the same day. There is usually a fee associated with CHAPS payments.. Payments out of the account can be made via Faster Payments, SEPA and Direct Debit.

The agency banking solution is provided via our partner Modulr and is fully integrated into the Thredd system. It is available to customers in the UK and EU.

1.2 How does it work?

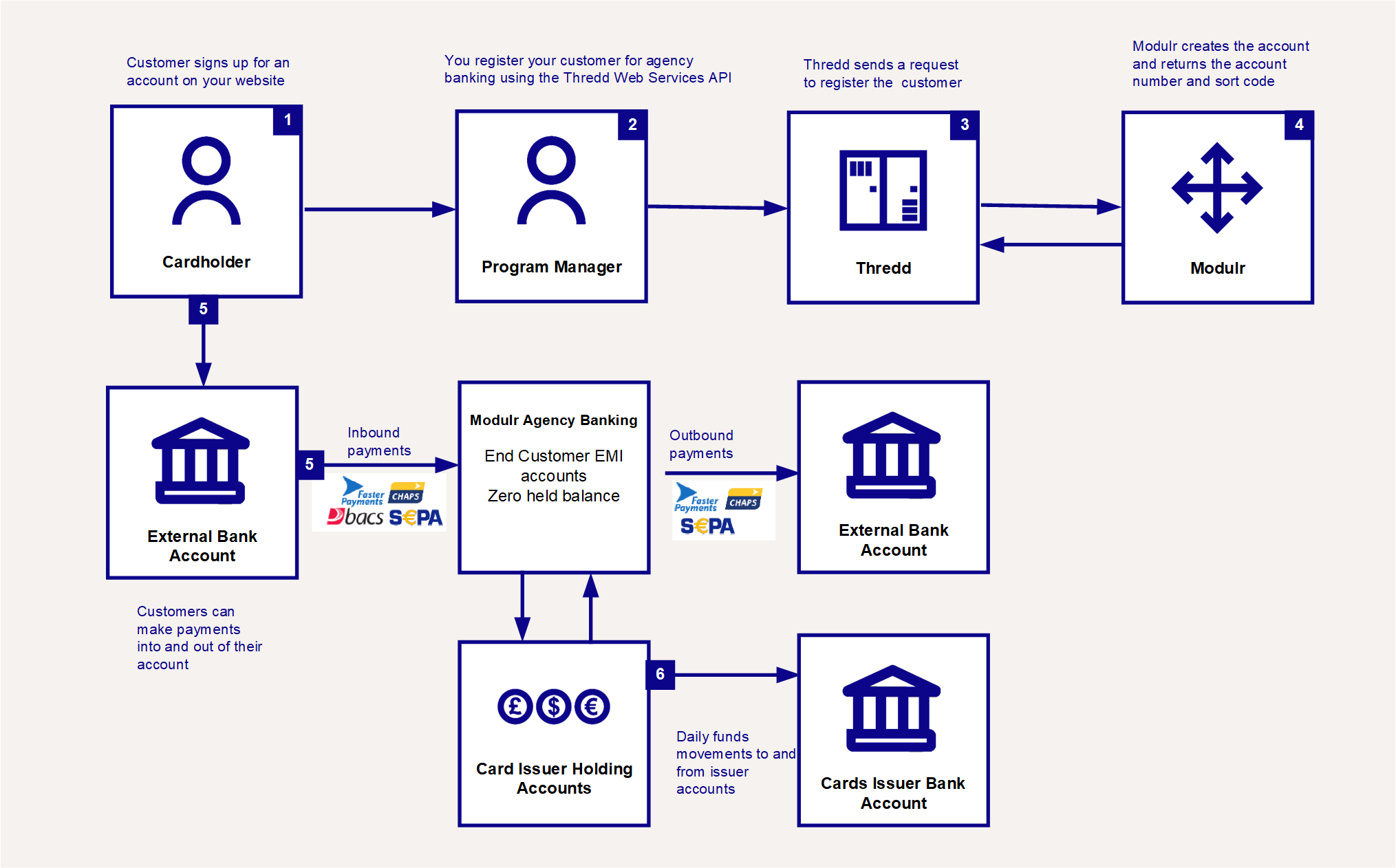

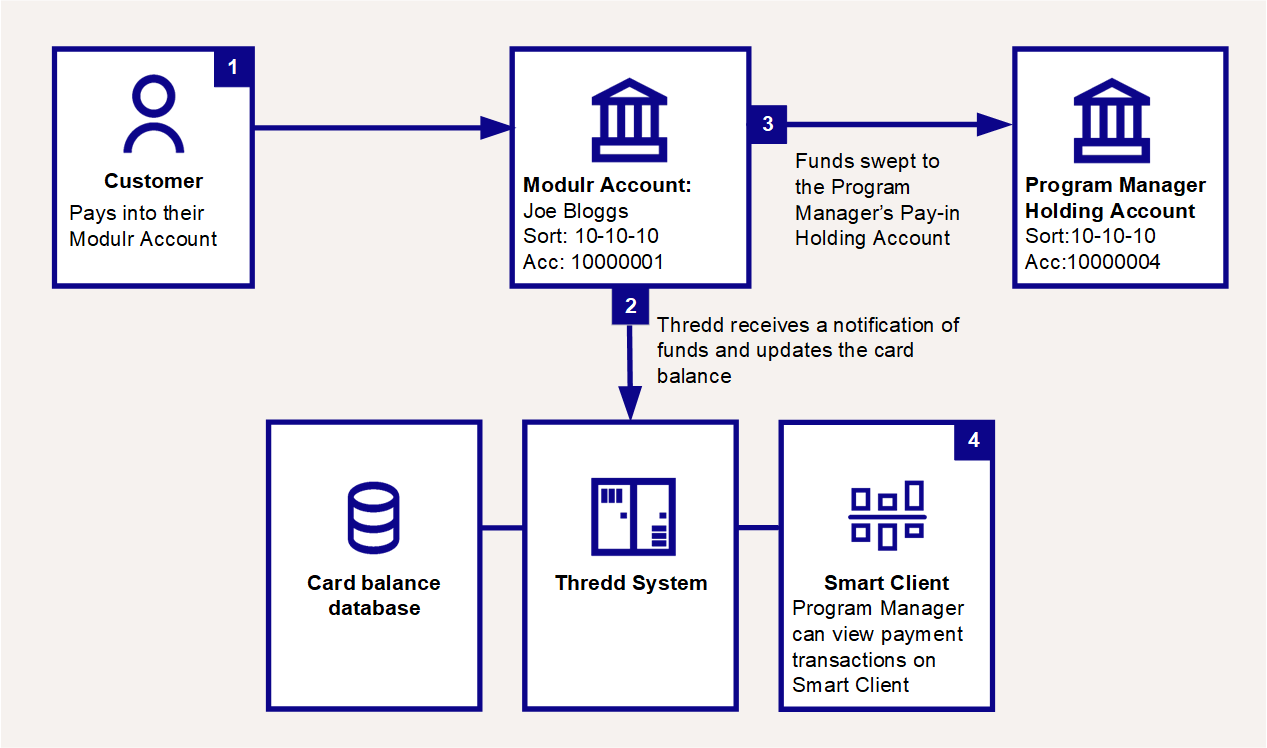

Figure 1 below provides an overview of how bank account registration and agency banking transactions work.

Figure 1: Agency Banking via Modulr

When we create a customer account on the Modulr system, the account is in your end-customer’s name, but customer balances are not stored in these accounts. Thredd acts as the system of record (i.e., Thredd accepts or declines card authorisations based on the balance record in the Thredd system). The card issuer holds the end customer funds – customers can make payments using their Modulr accounts.

Below are further details of the steps:

-

The customer signs up for an account on your website.

-

You use the Agency Banking web services API to register the customer for Agency Banking.

-

Thredd sends Modulr a request to register the customer.

-

Modulr creates the customer-named account and returns the account number and sort code.

-

Customers can make payments into or out of their account using one of the supported payment methods (e.g., Faster Payments, BACS, CHAPS or SEPA). Funds are moved into the Card Issuer holding accounts in Modulr, while Thredd maintains the balance ledger/system of record.

-

Funds are available in the Modulr holding accounts. Issuers can implement periodic or daily funds movements between their Modulr holding account and the issuer bank accounts.

1.3 Supported Agency Banking Features

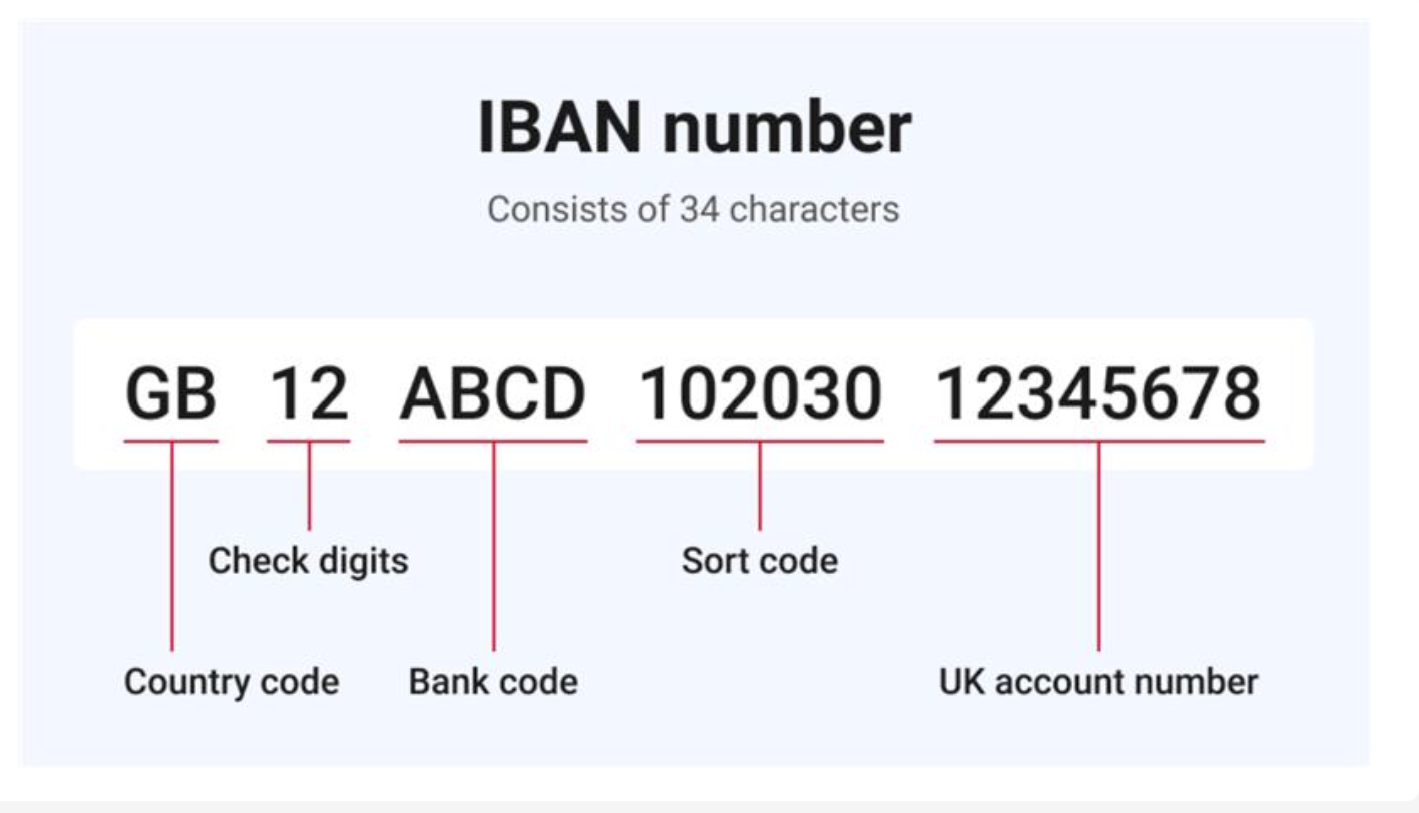

All registered customers are provided with a GBR or EUR bank account number, IBAN and sort code. The following payment methods are supported:

-

Faster Payments

-

BACS / CHAPS

-

SEPA (Single European Payment Area) payments

-

Direct Debit

1.3.1 Faster Payments

Typically, Faster Payments are used for peer to peer funds transfers.

The Faster Payment (FP) schedule is set up by the Program Manager.

-

Faster Payments In operate on true Faster Payment rails.

-

Faster Payments out are released according to the Program Managers schedule.

1.3.2 BACS

BACS (Bankers’ Automated Clearing Services) is a payment generally made in bulk to a customer account on a 3-day processing cycle.

BACS payments are traditionally the payment medium of corporate or government institutions (i.e., for payroll, pensions, benefits payments).

BACS payments happen daily and overnight.

1.3.3 CHAPS

CHAPS (Clearing House Automated Payment System) is typically used for one-off, high-value payments that need to be sent and received on the same day.

There is usually a fee associated with CHAPS payments (£25-£30). (BACS and Faster Payments are free.)

The majority of outbound payments are made via Faster Payments, but if this is a high-value payment (e.g., over a million pounds), we would process this via CHAPS.

1.3.4 SEPA Payments

The Single Euro Payments Area (SEPA) makes European payments as easy as payments made in the UK.

To do this the country code has been added to the IBAN to identify which country to send the payment to:

A SEPA payment takes about 24 hours, so is not as quick as Faster Payments.

European payments do not need to be signed up for with Agency Banking, but Agency Banking is needed if you want SEPA.

1.3.5 Direct Debit

Direct Debit is currently only available to customers on EHI Mode 3. Restricted to UK accounts only.

A Direct Debit is an instruction from a customer to their bank, authorising an organisation to collect payments from their account, as long as the customer is given advance notice of the payment amounts and payment dates.

Direct Debit is typically used for taking regular or recurring payments, such as household bills, subscriptions, memberships or charitable donations.

Direct Debit payments are not always for the same value.

1.4 Agency Banking Transaction Flows

This section provides examples of the transaction flows for customer banking registration and payments in and out of the account.

1.4.1 How to enable customer banking services

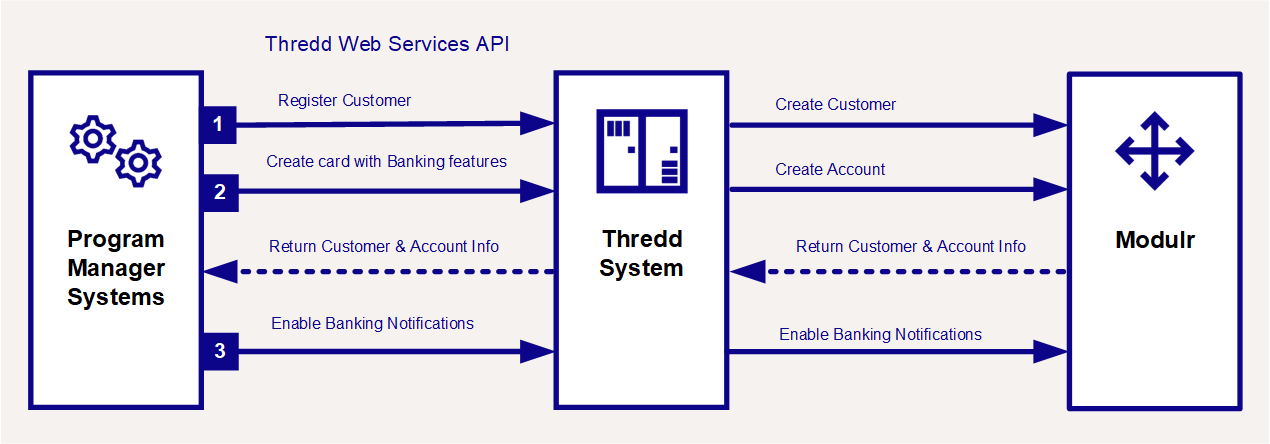

Figure 2 below describes the steps in setting up a customer for Agency Banking using the Thredd Web Services API.

Figure 2: Create Banking Services API

-

Register a customer for agency banking, using the

Ws_Banking_CreateCustomerAPI. This web service call creates a customer record on the Modulr system and returns a unique Customer ID that can be used in all Agency Banking web services API for subsequent actions. See Step 1: Registering a Customer for Agency Banking. -

Create a card with agency banking features enabled, using the

Ws_CreateCard_V2 API. This web service is similar to a Create Card web service. It creates a physical or virtual card with a linked banking account that can be used for banking payments. See Step 2: Creating a Card with Agency Banking -

Enable customer banking notifications, using the

Ws_Banking_RegisterNotificationAPI. This web services allows you to configure and enable notifications that can be sent to the customer or to your systems for various types of transactions, such as balance enquiries and information on payments into and payments out of the account. See Step 3: Registering a Customer for Banking Notifications

1.4.2 How do Payments In Work?

Figure 3 below shows how payments into the customer’s bank account (Via Faster Payments, BACS, CHAPS or SEPA) work:

-

The customer transfers funds into their Modulr Account using their unique Modulr sort code and account number.

-

Thredd receives a notification of the transferred funds and updates the available funds in the database (system of record) to include the payment in amount.

-

The funds are swept to the Program Manager’s payment holding account.

-

Payment transactions are displayed in Smart Client.

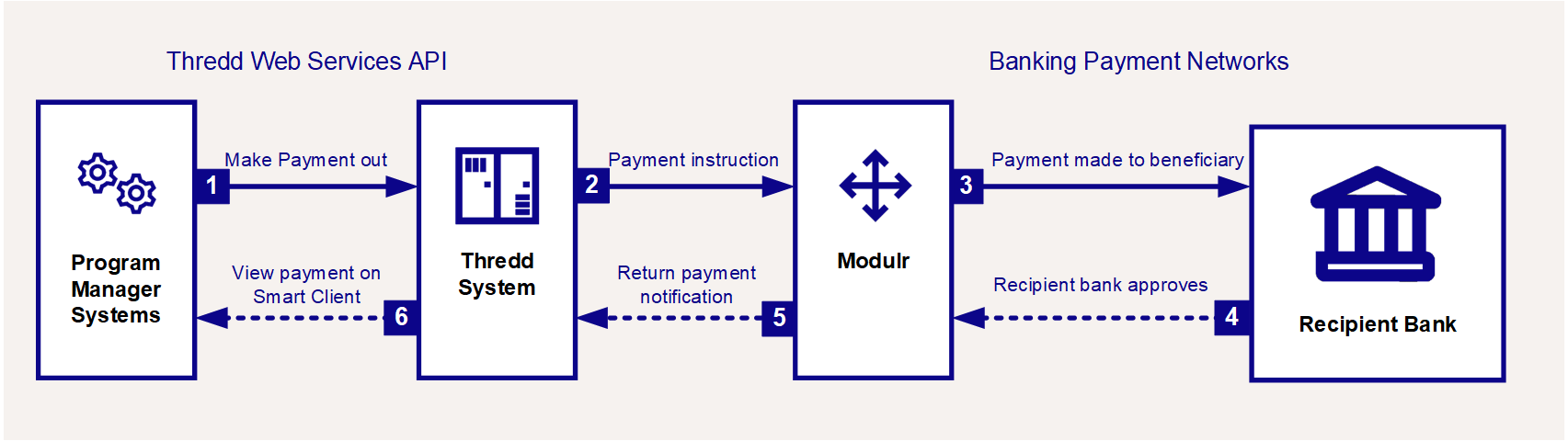

1.4.3 How do Payments Out Work?

Figure 4 below shows how payments out of the customer’s account (via Faster Payments, SEPA or Direct Debit) work:

-

Your systems make a payment out of the customer’s account using the Ws_Banking_TransferFunds API. Your call includes details of the account to take payment from and the amount, currency and recipient of the payment. See Making External Payments.

-

Thredd sends the payment instructions to Modulr.

-

Modulr makes the transfer to the beneficiary account using the banking payment network.

-

The recipient bank accepts the payment and returns a response to Modulr.

-

Modulr returns a payment notification to Thredd. Thredd updates its systems.

-

Payment transactions are displayed in Smart Client.