2 Steps in an Agency Banking Project

This section provides an overview of the steps in a typical agency banking project.

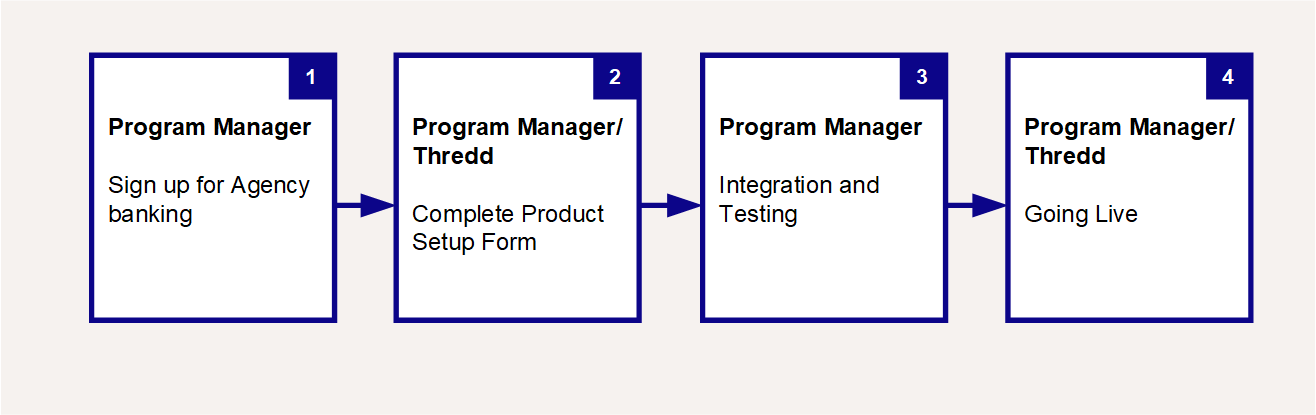

Figure 5: Steps in setting up Agency Banking

Each of these steps is described in more detail below.

2.1 Sign-up for Agency Banking

Let your Thredd account manager or Business Development Management know you are interested in this service. They will discuss costs and timescales with you and send you documents to complete.

Complete Pre-requisite Documentation

Make sure you have read and signed your Thredd contract, which will include details of the Modulr service and Thredd charges for using this service.

Your Thredd Business Development Manager will provide you with copies of the following documents which need to be completed:

-

Documents required for Know your Customer (KYC) and AML checks

-

Risk Assessment documentation

-

Modulr Information Requirements Form

Thredd will pass your completed documents to Modulr, for verification and account setup. If Modulr has any queries at this stage, your Thredd Business Development Manager will contact you to clarify.

If you are using the services of an Issuer, they will need to review and complete sections relating to the Issuer.

2.2 Complete your Agency Banking Product Setup Form

You will be assigned a Thredd Implementation Manager, to set up your account on the Thredd system. They will arrange an initial kick-off session to discuss your requirements and work with you to complete your Agency Banking Product Setup Form (PSF). For details, see Completing your Agency Banking PSF.

Once your form is completed, your Implementation Manager can set up Agency Banking in the Thredd Test Environment.

2.3 Integration and Testing

You can use Thredd Web Services to register your customers for Agency Banking and create cards with agency banking features enabled. For details, see Using the Thredd Web Services API.

Once you are familiar with how the Agency banking web services work, you can integrate them into your systems and test the web services in the Thredd Test Environment (UAT).

You can view all successful and failed transactions on Smart Client in the UAT Environment.

Thredd can test account creation and check the sort code format and 4th line embossing in UAT.

For more information on using Smart Client, refer to the Smart Client Guide.

2.4 Going Live

Once you have completed integration and you are ready to switch to the live production environment, notify your Thredd Implementation Manager, who will set up your account.

Before you release or enable the banking service for your customers, Thredd recommends that you put through some test transactions in the production environment, to test incoming and outgoing Faster Payments:

-

Make sure payments are reported as expected in Smart Client, in Thredd XML reports and EHI messages, and in your customer and Issuer bank accounts.

-

Test to ensure your call centre staff know how to manage failed payments, refunds and crediting of payment between accounts; see Managing Banking Payments .

2.5 Completing your Agency Banking PSF

Your Thredd Implementation Manager will work with you to complete your Agency Banking Product Setup Form (PSF). This form has three tabs:

01. Banking Issuer Details

02. Bank Institution Details

03. Velocity Limits

2.5.1 Banking Issuer Details

Select the type of banking services you want to enable at an Issuer level for payments in and payments out. Currently supported options include:

-

Banking IN — BACS, CHAPS and Faster Payments into accounts using the banking network

-

SEPA IN — SEPA Payments into accounts across Europe using the banking network

-

Banking OUT — Faster Payments out of accounts using the banking network

-

SEPA OUT — SEPA Payments out of European bank accounts using the banking network

-

Direct Debit — set up regular payments from the account. Restricted to UK accounts only.

Direct Debit payments is currently only available to customers on EHI Mode 3.

2.5.2 Bank Institution Details

Complete the following details:

|

Field |

Description |

||||||||

|---|---|---|---|---|---|---|---|---|---|

|

Institution |

Your institution name, as set up by Thredd. |

||||||||

|

Product |

The name of your agency banking product as set up by Thredd. |

||||||||

|

Banking Issuer |

Your issuer name or the name of your issuer. |

||||||||

|

Return Account Details |

Enable if you want the account number and sort code to be returned in the |

||||||||

|

Allocated sort code |

The sort code allocation by Modulr for making payments into the account |

||||||||

|

Preferred sort code style |

Select the format for the sort code on the card generation file. Options are:

|

||||||||

|

Issuer Account Number |

The account number of your issuer account, into which funds will be paid. |

||||||||

|

Issuer Sort Code |

The sort code of your Issuer account, into which funds will be paid. |

||||||||

|

Review Bank Transactions |

Enables Agency Banking transactions to be reviewed by the Issuer before being returned. |

||||||||

|

Banking IN |

Whether to enable BACS, CHAPS and Faster Payments into the account. |

||||||||

|

Banking OUT |

Whether to enable Faster Payments out of the account. |

||||||||

|

Direct Debit IN |

Whether to enable Direct Debit Payments into the account.

Note: Direct Debit is currently only available to customers on EHI Mode 3. |

||||||||

|

Direct Debit OUT |

Whether to enable Direct Debit Payments out of the account.

Note: Direct Debit is currently only available to customers on EHI Mode 3. |

||||||||

|

SEPA IN |

Whether to enable SEPA Payments into the account. |

||||||||

|

SEPA OUT |

Whether to enable SEPA Payments out of the account. |

||||||||

|

Modulr Banking |

Whether to enable Agency Banking via Modulr. Select Yes. |

||||||||

|

Modulr Product ID |

Your Product ID, as provided by Modulr. |

||||||||

|

Lower Limits Value |

The card Velocity Limits Group to use for your Modulr card product. This group determines the daily and single transaction amount payments limits that apply. See Velocity Limits. |

||||||||

|

Suspense Card |

The account to use for suspense payments (holding account contains payments where the recipient account holder cannot be identified; funds must be returned back to the sender if the recipient cannot be identified after 10 days) |

||||||||

|

Min Payment in Bypass |

Bypass the minimum Payment In threshold. |

||||||||

|

Modulr Holding Account ID |

Your holding account ID, as provided by Modulr. |

2.5.3 Velocity Limits

Limit Groups are set up for card products and can be used to control the frequency and amount of any transfers into or out of the account. In the product setup form, you can specify separate limit groups for payments in and payments out of the account.

At the time when you create a card with banking features, if you do not specify a Limit Group, then the default limit groups you have specified here for your agency banking card product will be used.

The table below shows the options that can be configured for each of the payment types (Pay_In and Pay_out) in the Limit Group.

|

Option |

Description |

|---|---|

|

Transaction Amount (limit applies per transaction) |

|

|

Maximum Per Transaction |

The maximum amount, in the account currency, of any single transaction. Transaction amounts above this threshold will be rejected. Example: 5000.00. The maximum value is 999999999.99. |

|

Minimum Per Transaction |

The minimum amount, in the account currency, of any single transaction. Transfer amounts below this threshold will be rejected. Example: 1.00. |

|

Daily Limit (limit applies per day) |

|

|

Daily Limit |

The maximum daily cumulative amount permitted, in the account currency. Transaction totalling above this daily threshold will be rejected. For example: 7000.00 per day. The maximum value is 999999999.99. |

|

Daily Frequency |

The maximum number of transactions allowed in a single day. For example, up to 5 transactions are permitted per day. The maximum value is 9999. |

|

Accumulated Limit 1 (limit applies over specified period, e.g., month) |

|

|

Accumulated Limit 1 |

The maximum cumulative amount permitted, in the account currency, over the defined period. Transactions totalling above the threshold for the defined period will be rejected. For example: 50000.00 per month (30 days). The maximum value is 999999999.99. |

|

Accumulated Frequency 1 |

The maximum number of transactions allowed over the defined period. For example, up to 200 transactions are permitted per month (30 days). The maximum value is 9999. |

|

Accumulated Period 1 |

The period over which the accumulated limit applies. For example: 30 days. |

|

Accumulated Limit 2 (limit applies over specified period, e.g., year) |

|

|

Accumulated Limit 2 |

The maximum cumulative amount permitted, in the account currency, over the defined period. Transactions totalling above the threshold for the defined period will be rejected. For example: 500000.00 per year (365 days). The maximum value is 999999999.99. |

|

Accumulated Frequency 2 |

The maximum number of transactions allowed over the defined period. For example, up to 2000 transactions are permitted per year (365 days). The maximum value is 9999. |

|

Accumulated Period 2 |

The period over which the accumulated limit applies. For example: 365 days |

Maximum Card Balance

This option enables you to specify a maximum balance that can be held in the card.

The maximum value is 999999999.99.